Jabotabek Is Not Indonesia: What Banks and Fintechs Get Wrong About Indonesia Youth Consumers

- RB Consulting

- May 30

- 5 min read

We surveyed 5,027 SMK students across 20 provinces in urban and semi-urban Indonesia. When we split the data by geographic area, we found not one youth market — but four, with meaningfully different financial realities. For any bank, digital bank, e-wallet operator, or fintech targeting this cohort, the strategic implication is direct: your Jabotabek playbook will not work in Java. Your Java playbook will not work in Sumatra. And none of them will work in the rest of Indonesia.

The Numbers That Make the Case

Let us start with e-wallet ownership — the most basic measure of financial product penetration in this age group.

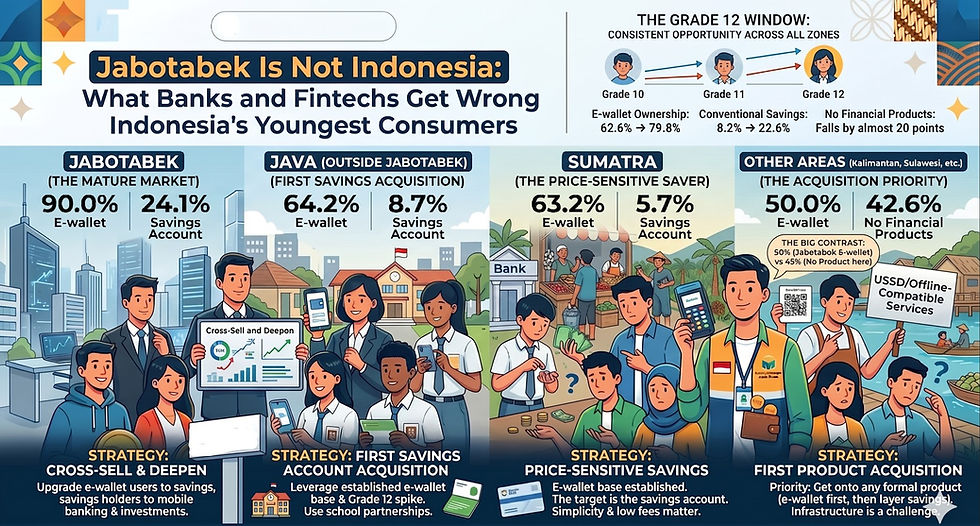

• Jabotabek: 90.0% of students own an e-wallet

• Java (outside Jabotabek): 64.2%

• Sumatra: 63.2%

• Other Areas (Kalimantan, Sulawesi, Bali, NTT, Maluku, Papua): 50.0%

Now look at the other end of the spectrum — the share of students who own no financial product at all:

• Jabotabek: 6.6%

• Java (outside Jabotabek): 31.3%

• Sumatra: 32.3%

• Other Areas: 42.6%

90% vs 43% E-wallet ownership in Jabotabek versus the share of students with no financial product at all in Other Areas of Indonesia |

These are not marginal differences. In Jabotabek, a bank or fintech is talking to a cohort that is already financially engaged — the conversation is about upgrading and deepening the relationship. In Other Areas, nearly half of the same age group has never opened any financial product. The starting point is different. The product needed is different. The channel is different. The message is different.

Running one national campaign that treats these four zones as a single market is not just inefficient — it means being irrelevant to at least three of them.

What Jabotabek Actually Tells You

The Jabotabek data is not just higher across the board — it reflects a structurally different financial ecosystem. With 90% e-wallet penetration and 24.1% conventional savings account ownership (compared to 5.7% in Sumatra and 8.7% in Java outside Jabotabek), Jabotabek students have already moved through the first two rungs of the financial product ladder.

For a bank operating in Jabotabek, the priority questions are not about acquiring the unbanked. They are about conversion and deepening: how do you move an e-wallet user to a savings account? How do you move a savings account holder to mobile banking and then to investment products? These are cross-sell and engagement questions, not acquisition questions.

The Jabotabek youth who already has a ewallet account and a bank savings account is a materially different customer from the student in Makassar who has never held any financial product. Treating them with the same offer is a waste of both marketing budget and opportunity.

The Grade 12 Window — Everywhere

One finding holds consistently across all four geographic zones: financial product ownership accelerates sharply in Grade 12. Compared to Grade 10 students:

• E-wallet ownership is up 17 percentage points by Grade 12 (62.6% → 79.8% nationally)

• Conventional savings account ownership nearly triples (8.2% → 22.6% nationally)

• The share with no financial products at all falls by almost 20 points (32.8% → 13.1% nationally)

Something changes in the final school year. Students approaching graduation — whether heading into the workforce or into higher education — begin opening accounts at a significantly faster rate than their younger peers. This pattern is consistent across all regions, even if the absolute ownership levels differ.

This creates a specific, time-bound acquisition opportunity. The student who has no savings account in Grade 10 has a 1 in 4 chance of opening one by Grade 12, without any intervention from a financial institution. With a targeted offer at the right moment — near the end of the school year, tied to graduation or first job anticipation — that conversion rate is almost certainly higher.

No bank or fintech in Indonesia currently has a structured Grade 12 acquisition programme. That is an open space.

The E-Wallet Is the Onramp, Not the Threat

Banks and conventional financial institutions often frame e-wallet adoption as competitive displacement. The data from the IYG Study suggests this framing is wrong — at least for this age cohort.

In Jabotabek, the region with the highest e-wallet penetration (90%), conventional savings account ownership is also the highest (24.1%). In Other Areas, where e-wallet penetration is lowest (50%), unbanked rates are the highest (42.6%). The two measures move in the same direction.

This is consistent with what financial inclusion research shows in other markets: the first digital financial product lowers the cognitive and behavioural barrier to the second. E-wallet adoption is not competing with savings account adoption — it is preceding it and enabling it.

For a bank designing a product strategy for this cohort, the implication is clear. The most efficient customer acquisition path is not through a standalone bank account launch. It is through partnership with or embedding within the e-wallet ecosystem that these students already trust — particularly outside Jabotabek, where formal banking has not yet achieved the penetration that e-wallets have.

Four Different Markets, Four Different Plays

Based on the IYG Study data, we would characterise the four geographic zones as requiring fundamentally different commercial strategies:

Jabotabek: Cross-sell and deepen. Students are already partially banked. The conversation is about upgrading e-wallet users to savings, and savings holders to investment and mobile banking.

Java (outside Jabotabek): First savings account acquisition. E-wallet base (~64%) exists. The Grade 12 spike creates a natural window. School-based or employer-partnership activation is the most efficient channel.

Sumatra: Similar profile to Java, but with even lower savings penetration (5.7%). E-wallet base is established. The savings account is the target product. Price sensitivity is higher and product simplicity matters more.

Other Areas: First product acquisition. With 42.6% owning nothing, the priority is getting students onto any formal financial product — e-wallet first, then savings layered on top. Infrastructure constraints are real; digital-only solutions will not reach everyone.

The Strategic Takeaway

The IYG Study is a study of SMK students — Indonesia's youngest active consumer cohort, aged 15 to 18, on the verge of independent financial decision-making. The data is nationally representative across 20 provinces and post-stratification weighted.

What it shows, clearly, is that Indonesia's youth banking market is not one market. The Jabotabek assumption — that what works in the capital works everywhere — is the most common and most costly mistake in financial services marketing in this country.

Understanding where your customers actually are on the financial product ladder, and what the next logical step is for each of them, is the prerequisite for any strategy worth the name.

This post draws on the IYG Study 2026 by RB Consulting — a quantitative study of 5,027 SMK students across 20 provinces in Indonesia. The full report includes four commercial angles for banking and financial services clients, with subgroup analysis by gender, grade, and geographic area. For banks, digital banks, e-wallet operators, and fintechs interested in a deeper analysis of this cohort — or bespoke research among your specific target market — please get in touch. Contact: iwanmurty@rbconsult.co · +62 812 100 8550 · www.rbconsult.co |

→ Also read: 6 in 10 Young Indonesians Would Save First. So Why Does Only 1 in 8 Have a Savings Account?

Comments